Boost Your Income With These 25 Lucrative Side Hustle Ideas

Almost everyone has a financial goal: from paying off a vehicle loan to bankrolling a once-in-a-lifetime vacation, getting rid of credit card debt, and beyond.

However, it can be challenging to find an additional income source that doesn’t conflict with your full-time job.

Luckily, there are many types of side hustles that can boost your income without compromising your work day. Whatever your priority, whether it’s passive income or a creative outlet, you can find a money-making option that meets your needs.

In this article, we’ll look at the current state of the gig economy that makes many side hustles possible. Then, we’ll dive deep into 25 lucrative side gigs you can try out to build one or more additional streams of cash flow.

What You Need To Know About The Gig Economy

In our connected digital world, there are many opportunities for side hustles.

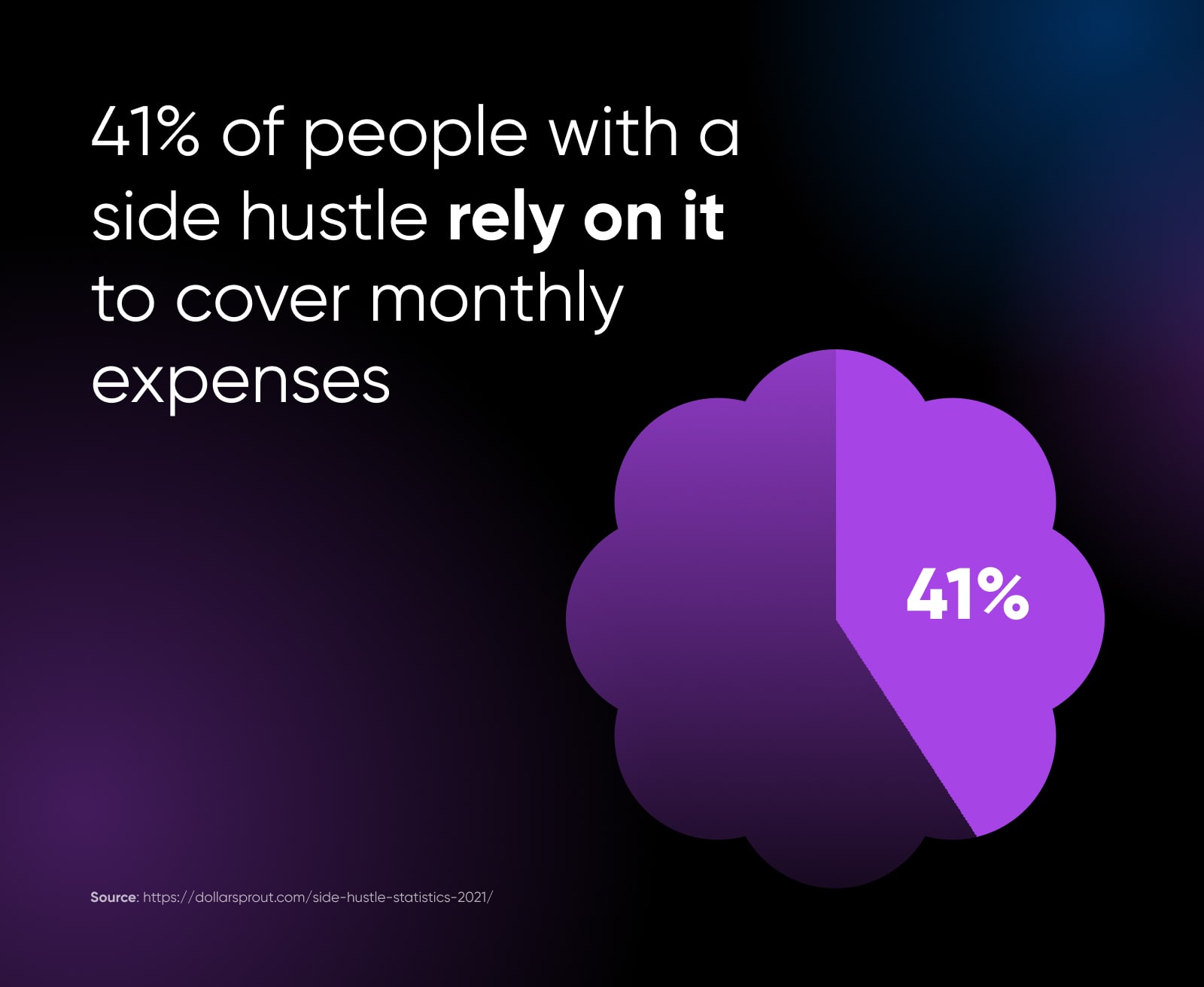

Part-time gigs are even becoming a permanent solution for many people. In fact, more than a third of gig workers have come to depend on income from their side hustles.

People from all generations are currently taking advantage of gig work because of its flexibility and earning potential. Side hustles can offer extra income for spending, saving, or covering living expenses.

That means right now is a perfect time to strike out on your own with a side hustle. Not only can this path be rewarding in many ways, but it may even improve your performance at your day job.

Intrigued? Then come along to explore dozens of options.

25 Lucrative Side Hustle Ideas

There is no shortage of opportunities for building a lucrative side hustle — both online and off.

Let’s investigate some accessible and rewarding options!

1. Sell Graphic Design Services

If your friends are always asking you to create signs, posters, or logos, you might want to pursue graphic design.

Graphic design is a diverse field, so you can choose a niche related to your strengths. Whether designing products, websites, or branding, this side hustle can bring in many clients that require your services.

To get started, you’ll want to set up an online portfolio. This is a digital resume that displays your design services and previous work.

When looking for graphic design jobs, you might also consider using an online marketplace such as Creative Market. Unlike platforms like Etsy or eBay, Creative Market is designed for creative digital products and services.

With Creative Market, you can set up a digital storefront to market your web themes, fonts, or templates. Using this platform, you can set your own prices and display your graphic design work to more than a million potential clients.

2. Become A Virtual Assistant

From appointment scheduling to inbox assistance, there is a wide array of tasks that busy professionals need help with. As a virtual assistant (VA), you can assist your clients with their small business outsourcing needs.

Working as a VA can be a great option if you’re a stay-at-home parent or even a college student looking to bring in a little extra cash. In many cases, VA work will involve skills you already have, such as typing, emailing, or social media management.

Striking out on your own can be daunting, but you can use a freelancer website like PeoplePerHour to get started. Here, you can find new projects, set your rates, and enable clients to hire you.

Just be aware that being a VA requires excellent time management. Also, you’ll have to be willing to hustle for each client if you want to make it in this professional space.

3. Create A Proofreading/Editing Service

If you enjoy helping others improve their written content, starting up a proofreading and editing service can be very lucrative. This side hustle includes tasks like fixing spelling, grammar, and other errors before a business or individual publishes their content.

This is another side hustle perfect for college students. You can work out a schedule that meshes well with your classes and put that sentence diagramming skillset to use. You can even set up a simple freelance writer website to describe and highlight your previous work, qualifications, and services.

Don’t have any work just yet? Pretend one of your favorite businesses or authors is a dream client, and use your website to post examples of how you would improve upon content they’ve already published.

Find work opportunities by surfing writing and freelancing-focused subreddits. You can also look for businesses that are hiring editors on LinkedIn and pitch them your services on a freelance basis. They get their tasks covered, and you get to maintain your flexibility — it’s a win-win!

If you’re working from home as a proofreader, you can deduct many household items from your taxes. Just remember that you’ll need to keep a diligent record of your work expenses and hours.

Get Content Delivered Straight to Your Inbox

Subscribe to our blog and receive great content just like this delivered straight to your inbox.

4. Open An Amazon Storefront

The online retail giant Amazon enables entrepreneurs to create storefronts on their website. If you have a product to offer, you can set up a seller account with Amazon and potentially access billions of worldwide visitors.

One of the most intriguing things about using an Amazon storefront as your side hustle is that it has many profitable options. For example, selling private-label products can earn you $5,000 in monthly revenue. Alternatively, you could also sell handmade items or print-on-demand products.

There are sometimes fees associated with Amazon’s services, so you’ll have to research the options and decide what works best for you. Additionally, you’ll need to handle shipping yourself unless you go all in and use Amazon’s fulfillment service.

5. Offer Errand Services

Errand-running has become a big business. Grocery pickups and fast food delivery are two of the most popular options, with online food delivery worth more than a cool trillion as of 2023.

You can easily profit from this popular market by starting an errand-running business in your down time. By signing up for a food delivery service, you can start making money within the first few days.

You’ll need to check your local regulations to ensure you have the right kind of insurance coverage for this side hustle. Additionally, you may have to work extra vehicle maintenance into your overall budget.

However, if you have a reliable vehicle and like to interact with people while running errands, this is an opportunity worth considering.

6. Drive For A Rideshare Company

In the same vein as errand-running, driving for rideshare companies can be very lucrative as a side hustle. Uber drivers in the U.S. can make around $38,000 a year, but the income vastly depends on location and your availability.

Driving for Uber allows you to set flexible hours so that you can work around your full-time job. Additionally, you’ll receive a base fare for every ride, plus extra tips from riders.

Of course, offering driving services means picking up strangers — which can be risky for a whole host of reasons. So, while almost anyone can try this lucrative side hustle, it’s a job to consider carefully.

You’ll also want to understand the company’s safety policies and what to do in specific situations. However, if you generally like meeting new people and driving around town, this could be an excellent option for you.

7. Start A Repair Service

Simple home repairs and “handyperson” jobs are possible side hustles to consider if you have a good set of tools and like fixing things. You’ll only need basic repair knowledge with a repair service side gig.

You can utilize a website like Taskrabbit when building up a good reputation. Using this platform can be an easy way for clients to find you and hire you for specific projects.

With each season, you can create new, marketable services for your business. For example, you can offer holiday decoration services for people who can’t string up lights easily or gutter cleaning in the fall and spring.

8. Design WordPress Websites

Roughly 252,000 new websites are created every day. That makes for a steady stream of potential clients for a website design side hustle.

If you’ve got the skills, designing websites is lucrative enough that you can select the clients you want to partner with and only work the hours you choose. Plus, working with a user-friendly content management system (CMS) such as WordPress makes it easy to create functional, beautiful websites.

Content Management System (CMS)

A Content Management System (CMS) is a software or application that provides a user-friendly interface for you to design, create, manage, and publish content.

Read MoreNot only is WordPress the most popular and widely-used CMS on the market, but it’s also open source. This means there’s a lot of versatility when building with it.

All in all, this option is a great one for anyone with some web design knowledge. You can use page builders and other tools to create a business quickly without even needing extensive coding abilities.

9. Develop And Sell Themes/Plugins

When it comes to WordPress and side hustles, there are other options besides designing entire websites. As we mentioned previously, WordPress is built on open-source software. This means that if you do have sufficient coding knowledge, you can easily develop new WordPress plugins and themes.

After developing your first WordPress theme or plugin, you can submit it to the WordPress team to see if it meets their guidelines. After approval, you can offer a basic, free version of your product. Then, you can entice people to buy a premium version with advanced features.

If you’re just starting and want to test your skills, we have a wealth of WordPress tutorials and walkthroughs to help you along the way. Using resources on GitHub, an open-source code repository, is another excellent method for learning the ropes.

Theme

A WordPress theme is a layout tool that enables you to change the design of your site. A theme is composed of a group of files within a zipped folder that includes page templates, CSS stylesheets, images, and more.

Read More10. Create An Affiliate Blog

Since tons of brands have affiliate marketing programs, delving into this industry can be an excellent way for bloggers to make a passive income. This lucrative side gig offers low start-up costs, unlimited product choices, and little management.

Getting started with affiliate marketing is a great way to monetize your website.

With affiliate marketing, an independent blogger — that’s the affiliate — promotes a brand’s products. When you become an affiliate, you earn commissions by directing traffic to a business’s website or storefront. Essentially, you’re rewarded for writing about and recommending products to your followers.

One of the most popular affiliate programs for bloggers is Amazon Associates. Since Amazon has many products to choose from, you can easily find ones that fit your niche.

Although affiliate marketing can have many benefits, it’s essential to market products effectively. You’ll want to recommend goods that align with your audience. For instance, if you’re starting a fashion blog, you can promote clothes from Amazon.

Finally, make sure you avoid spamming your audience with affiliate links. You’ll want to naturally incorporate affiliate products into blog content to maximize credibility. Additionally, you should provide an affiliate link disclosure to inform your audience.

Check out DreamHost’s affiliate program for an example of a well-executed affiliate plan in action.

11. Sell Handmade Items On Etsy

There are plenty of places to sell items online, but Etsy is one of the most popular options. Unlike other marketplaces, Etsy is slightly more focused on handmade items such as clothing, jewelry, and physical and digital art.

Etsy shoppers often focus on personalized items for gifts. With nearly 90 million active buyers globally as of 2023, you are very likely to find the right audience for your handmade products on Etsy.

When it comes to being successful on Etsy, reliable customer service can go a long way toward building a following. Posting quality photos and using search engine optimization (SEO) techniques can also help. You’ll also want to make sure you have a marketable product, of course.

Potentially the biggest challenge to creating a successful Etsy store is the level of competition. You’ll want to do your research on how to stand out. With that being said, Etsy is an excellent option for crafters and creatives of any type.

12. Start A Cottage Food Business

Another great way to have fun and bring in extra income is with a cottage food business.

Cottage food laws vary from state to state, so look to them to make sure what you make in the home can be sold at farmer’s markets, in shops, or online.

If you’re everyone’s go-to friend for cakes and confections, you might want to consider setting up a food blog or promoting your cottage food items on a platform such as TikTok or Instagram. By posting content consistently, you can develop a dedicated following that loves to see your baking process.

The only downside to cottage food endeavors is that it’s limited by how much time you can devote to cooking and baking, the cost of ingredients, and changing food regulations.

13. Set Up A Consulting Service

If you’re more of a “big picture” kind of person, you can always set up a consulting business. This lucrative side hustle can cover a wide range of professional areas and draw on skills you already have from your day job.

You’ll want to clearly establish your experience and expertise in the category you’re offering consulting services for. It might involve marketing, business development, technology, or sales.

To present a more professional image, you can use LinkedIn. By creating a LinkedIn company page, you can display your business resume and explain what you can offer to potential clients.

This is also a situation where your portfolio will matter a lot. Potential clients will want to know if you have the experience necessary to guide them in their business practices.

Keep in mind that to start a successful consulting gig, you’ll want to put together a clear outline of the agreed-upon work for each client. All parties must be on the same page regarding what a consult will include.

14. Become A Freelance Writer

Freelance writing is an increasingly popular option for a side gig. Nearly every website has a blog, but not every site owner is a skilled writer. Also, many people might not have the time to research and write posts consistently.

As a solution, many business owners outsource these tasks to freelancers. Additionally, lots of big marketing departments and agencies use freelancers to help with heavy workloads. You can reach out to companies like these directly or browse for work on sites such as the ProBlogger job board.

To help you land clients and brand yourself as a professional, you’ll want to ensure that you have a top-notch writer website. Here’s an example from freelance writer Michelle S. Loyd.

Your website should host your portfolio and provide details about rates and contact information. It can position you as an expert in your niche, whether that’s WordPress, tech, travel, fashion, or something else entirely.

Related reading How to Create a Freelance Writer Website

15. Resell Thrifted Items

A simple way to make extra money is buying items from a thrift store and reselling them. This process could involve finding a vintage piece, restoring it, and listing it for sale online. Alternatively, you could look for desirable items from prominent brands.

Some of the most profitable thrift store finds are textbooks, brand-name clothes, glassware, and record players. When you find these items, you can sell them for a profit on online marketplaces, flea markets, or your website.

eBay is a popular platform for secondhand items because you can sell almost anything. With millions of users worldwide, eBay’s platform can provide more visibility than a personal website.

Although you can list items using a personal account, eBay also allows you to create an online store. This setup gives you access to more listings with fewer fees.

Related reading: How To Accept Payments Through Your WordPress Website

16. Manage Social Media Posts

If you’re great at networking and multi-tasking, becoming a social media manager might be the right side hustle idea for you. In this position, you’ll be responsible for creating posts, analyzing traffic, and moderating comments across various social media platforms.

To set you apart from the competition, you’ll need to master a social media strategy that takes every platform and algorithm into account. You can do this by keeping your personal accounts up-to-date and following successful social media users. These methods can help you learn marketing strategies and significant trends quickly.

Social media management often requires juggling many different accounts and posting schedules. Although this job can be overwhelming, you can use applications such as Hootsuite to keep track of all your essential tasks

Hootsuite is an all-in-one social media management dashboard where you can create, preview, and schedule posts. You can also monitor previous post performance and analytics. Just remember to keep all the accounts you work with separate and establish a clear set of terms and conditions with your clients.

17. Become An Online Tutor

With an online tutoring job, you can access flexible hours and unlimited clients. Students are almost always looking for homework help, so this side gig could be ideal if you love teaching.

Although tutoring income can vary based on experience, this side hustle generally has high rates. Tutors can make anywhere from $15 to $125 per hour. If you are a qualified teacher and decide to teach older students, you can usually command a higher rate.

Out of the many online tutoring platforms available, Tutor.com is one of the best. When you sign up, you can create your schedule and even do unscheduled tutoring sessions if you need them.

Especially if you received higher education, becoming a tutor can put your skillset to good use.

18. Convert Your Spare Room Into An Airbnb

Many people decide to find full-time roommates to help pay their monthly expenses. However, listing your spare room on a platform like Airbnb can be a better alternative. This lucrative side hustle enables you to monetize your empty space while still living alone a good chunk of the time.

For a private room, the average host earnings in 2021 were a whopping $5,260

As an Airbnb host, you can decide which dates and times people can book your room. Plus, guests are only there for a short time, so this setup causes less wear and tear on your house.

Many owners list their homes on Airbnb, so it’s important to make yours stand out. You can get more bookings if you feature clear, detailed pictures and keep your home clean. Additionally, you should be communicative with guests and anticipate their needs to ensure that they leave good reviews.

Be warned, this side hustle of course involves inviting strangers into your house. This comes with risks, including stealing and loud, destructive parties.

19. Start A Podcast

Podcasts can be surprisingly lucrative. Thanks to sponsorships, advertising deals, and affiliate sales, it’s possible to earn a solid income while diving deep into your favorite subjects.

Getting started with podcasting is easy enough. Ideally, you’ll want to invest at least a little into equipment (such as microphones and editing software) to produce the best quality recordings. You’ll also likely need a dedicated hosting plan capable of handling high traffic so that your content won’t slow down your website.

The catch is that you’ll generally need to build up a regular audience to start seeing much income from podcasting. A good first goal to shoot for is 1,000 downloads per week — this is where you can begin to start making money from affiliate marketing and viewer donations.

20. Become A Transcriptionist

As a transcriptionist, you listen to recordings and turn them into written documents. All the gear you need to succeed in this position is a computer, fast internet connection, and word processing software.

Anyone can become a transcriptionist with the right skillset. Good typing skills, hearing and comprehension, and correct grammar are some of the basic requirements employers will look for. Your experience level likely won’t matter if you excel in these areas.

Rev is an online transcription company where you can sign up to become a freelancer. The average payout on Rev per month is $245.

To start transcribing with services like Rev, you’ll usually need to take a quiz and submit a transcript. You’ll be approved after this basic test, and then you can choose specific jobs you’d be interested in.

The best part about being a transcriptionist is its flexible work schedule. You can see deadlines, audio content, and pay before you sign up for a job. This way, you can focus on transcripts that are worth your time.

21. Get Paid For Dog Walking

Walking dogs can be a rewarding and flexible side hustle for animal lovers!

The primary skill required for dog walking is a good understanding of canine behavior and basic training techniques — or a willingness to learn them. Additionally, strong communication skills are essential when dealing with both dogs and their owners.

Several apps have emerged to connect dog owners with reliable dog walkers. Popular platforms like Rover and Wag! provide a platform for dog owners to find and schedule dog walkers. These apps often include payment systems, making the entire process convenient for both the walker and the pet owner.

Speaking of payment, the income potential for dog walking will vary a lot depending on factors such as location, demand, and the size and number of dogs you’re dealing with at once. On Rover, the average dog walk runs around $15 per walk. If you’re interested in adding on any services, such as pet sitting, you can grow your income potential.

22. Take Online Surveys

Taking online surveys is an increasingly-popular side hustle that’s especially suited for people who are looking for flexibility and convenience.

One of the main advantages of online surveys is that they don’t require specific skills or expertise. As long as you have a device, an internet connection, and some spare time — you can participate in this side hustle!

That said, patience and consistency are valuable traits as the payout for each survey can be relatively small with a few dollars, or less, of compensation per completion. However, if you’re able to find a platform that pays hourly, you could earn around $26/hour.

Several platforms and apps connect individuals with companies looking for survey participants. Some well-known survey platforms include Swagbucks and Survey Junkie. These platforms often offer a variety of opportunities, including market research, product feedback, and opinion polls.

23. Sign Up For User Testing

User testing is a side hustle where you can earn money by providing feedback on websites, apps, and products.

User testing typically involves navigating through a digital experience while recording your steps, thoughts, and any issues you come across. The compensation per test ranges — According to a review of UserTesting.com, the average pay per test comes out to $10. But, it all depends on the complexity and length of the task — and the expertise of the tester.

While no specific skills are required, having good communication skills to articulate your thoughts can enhance the value of your feedback. User testing is open to a wide range of people, from tech-savvy individuals to those with varying degrees of online proficiency.

UserTesting.com and Trymata are popular platforms that connect testers with companies seeking feedback. To get started, users typically need to sign up on their testing platform of choice, complete a demographic profile, and, in some cases, complete a sample test to demonstrate their testing abilities to better match them with well-fitting jobs.

24. Sell Online Courses

Have expertise in a particular subject or skill? If you can turn it into a course, you can sell it online! This hustle can be particularly appealing for educators and professionals looking to monetize their expertise outside of the typical work experience.

This side hustle may require more skill than some others. Aside from expertise in the subject matter you plan to teach, effective communication is crucial for delivering educational materials in an engaging manner. You also need enough technical skills to use your chosen tooling to create and edit the course content. An understanding of online marketing can also be beneficial for reaching a wider audience.

Several platforms and apps facilitate the creation and sale of online courses. Popular options include Udemy and Skillshare. These platforms provide tools for course creation, hosting, and marketing so you can focus on the content rather than the technical aspects.

Successful course creators can earn a significant amount over time. Some generate thousands or even millions of dollars in revenue! Vasco Cavalheiro for example has generated close to two million dollars selling courses on software development via Udemy and their own website!

25. Start A Dropshipping Business

Dropshipping is a retail practice where a seller doesn’t keep what they sell on hand, but has products shipped directly from a third party to a customer upon purchase.

It’s a good income stream for entrepreneurs looking to venture into e-commerce without dealing with inventory management and significant upfront costs.

While dropshipping offers flexibility and low entry barriers, starting a dropshipping business requires dedication and effort to stand out in a competitive market.

Dropshippers tend to make 20% to 30% on each sale, so your income is dependent on pricing and how many sales you’re able to make through marketing and retention strategies.

Several platforms and apps facilitate dropshipping businesses, such as Shopify and WooCommerce. These tools streamline the process of setting up an online store and automating order fulfillment.

Quick Tips: How to Set Yourself Up To Launch A Side Hustle

There’s a reason that getting a supplementary job like the ones listed above is called a hustle.

Adding a whole ‘nother job to your plate takes a lot of energy and ambition — and a thoughtful approach if you want to avoid burning out before you become successful.

Whatever your goals might be, there are several keys to setting yourself up for success when launching a side hustle. You’ll at least want to have:

- A clear outline of your objectives, and ideally a list of tasks to get you there

- Very solid time management skills

- A website with secure and trusted hosting so a spike in traffic and sales doesn’t lead to a blackout

- The ability to maintain good financial records (a connection with a financial advisor or tax specialist is a huge bonus!)

There are so many helpful resources available online that have endless time and space to teach you all about starting a side hustle. If you’re intrigued, we highly recommend seeking those out.

If nothing else, we hope this guide has at least convinced you that there’s no better time than now to take a chance on something you’ve always wanted to do!

Answering Your FAQs About Side Hustles

Now, let’s clear up some of the top questions many people have about side hustles.

What Is The Number One Side Hustle Right Now?

In 2024, some of the side hustles that are most heavily recommended across the internet include selling digital products (like courses!), taking online surveys, and freelancing in your particular area of expertise — writing, developing websites, graphic design, bookkeeping, video editing, decorating, and on and on.

Do Side Hustles Actually Work For Anyone?

In short, yes — side hustles can absolutely make you money (that’s what you mean by “work,” right?).

Need inspiration? We’ve got bucketloads.

Follow these ten social accounts to grow your business by following examples of how real people turned freelancing, course creation, podcasts, social media, and more into highly successful sources of income.

How Much Can I Make Per Month?

We hate to say it, but how much you make via your side hustle truly depends.

Any side hustle has the potential to be lucrative — or a total flop.

The best way to ensure that you’re able to eventually generate your desired income from a side hustle is to make sure it combines each of these factors:

- A high level of personal, demonstrable expertise

- Modern, in-demand skills

- Focus on a specialized/niche industry

- Creative marketing for a highly-targeted audience

How Do I Choose The Right Side Hustle?

The best side hustle for you will be contingent upon your individual skills, available resources, and dreams and goals.

For example, tutoring and selling handmade crafts may be best for a “people person” while tech-savvy individuals may find the most success by moonlighting in website building and management, e-commerce, and user testing.

Passion for something like, say, writing? Affiliate blogging and freelance writing may give you an outlet to monetize those authorship dreams.

Finally, think about the time and/or money you have to devote to a side hustle. Starting a podcast requires an up-front cash expenditure to get off the ground, but a side hustle such as creating courses costs little more than time during the set up phase.

Is My Side Hustle Income Taxable?

Yes, income from a side hustle will very likely be subject to taxation.

First, yearly earnings exceeding $600 from gig work are taxable.

Additionally, operations that aim to make a profit are considered to be businesses, while operations that exist simply for pleasure are considered hobbies. Business earnings are taxable. If your side hustle passes the hobby test (which it shouldn’t, if your goal is to make money) earnings may not be taxed. However, if you receive a Form 1099-K from a digital marketplace or payment app — which you could if you make $600 or more in a year — you are required to report and pay taxes on that income.

We highly recommend treating your side hustle as a business with taxable income and keeping good records throughout the year to make life easier when tax time comes.

Need Help Unlocking Your Earning Potential? Start Here

A side gig can give you a greater sense of freedom and active control over your life. Plus, it never hurts to earn a little extra cash now and then!

Set yourself up for a successful new side hustle by exploring your options, understanding your passions, getting realistic about your resources, and building a trustworthy online presence.

Whatever your hustle, DreamHost is here to help support you. With our unique business name generator, easy domain name registration, and professional website design, development, and management services — we can get you one step closer to successfully kicking off a lucrative side hustle!

Become a DreamHost Affiliate

Join the DreamHost Affiliate Program to get cash quickly. Earn up to $200 per referral!